October 12, 2019//-We tend to think of the topic of life insurance as morbid. After all, it’s an insurance policy that pays out when you pass away, but the big question here is what is the Best Age To Get Life Insurance Ohio? We will answer this question below on this article.

October 12, 2019//-We tend to think of the topic of life insurance as morbid. After all, it’s an insurance policy that pays out when you pass away, but the big question here is what is the Best Age To Get Life Insurance Ohio? We will answer this question below on this article.

However, when thinking of life insurance, we should really be focusing on how its primary function is to ensure those who depend on you will be safe and secure in the event you die.

In this sense, purchasing a life insurance policy could be considered a grand gesture. It’s an example of making a small sacrifice in the present to help your loved ones in a future without you.

This gives life insurance an emotional component that we don’t see with other types of insurance.

However, just because purchasing life insurance makes you feel warm and fuzzy inside, you still need to mind how you’re spending your money.

But as is the case in most of the insurance world, the details surrounding life insurance are abundant and confusing, and this can often lead you to overpay for things you don’t need, or worse, to not have enough coverage when you need it most, if you want to avoid the headache and avoid a bad call we recommend finding financial advisor.

To help you understand if you’re getting a good deal on your health insurance, we’ve dissected everything that goes into the premiums you pay, and we’ve also identified some national averages so that you can see if you’re paying more than you should.

We think it’s better to get a Contractor Cover to simplify your insurance buying process further than any other insurance brokerage and stop worrying about your insurance and keep track of multiple packages. Talking to Newport Beach life insurance litigation attorneys could be something one could do before going ahead with purchase of a life insurance.

Life Insurance Costs at a Glance

Return on Premium

Another variation of term life insurance is Return on Premium. With these policies, the insurance company actually gives you some or all of the premiums you paid into the policy if the term ends without you dying.

However, for this to make sense for the insurance company, they need to charge you higher premiums, as they will need to invest it in such a way that they can not only cover your benefit but that they can also pay you back at the end of the premium.

When you think about it, a Return on Premium policy is a way of paying yourself back when you’re older for an insurance policy you’ve bought now. It could be nice to get these premiums back, but in the event you don’t make it to the end of your term, you will have paid considerably more for what amounted to a traditional term life insurance policy.

Whole Life Insurance

After term life insurance, the next option you have is whole life insurance. As the name suggests, these types of policies cover you not just for a set term but rather your entire life. Whole life insurance policies are also different because they come with a savings account component.

Essentially, when you pay premiums, the insurance company invests that money for you intending to grow your account large enough so that it will cover your death benefit in the event your beneficiary needs to make a claim.

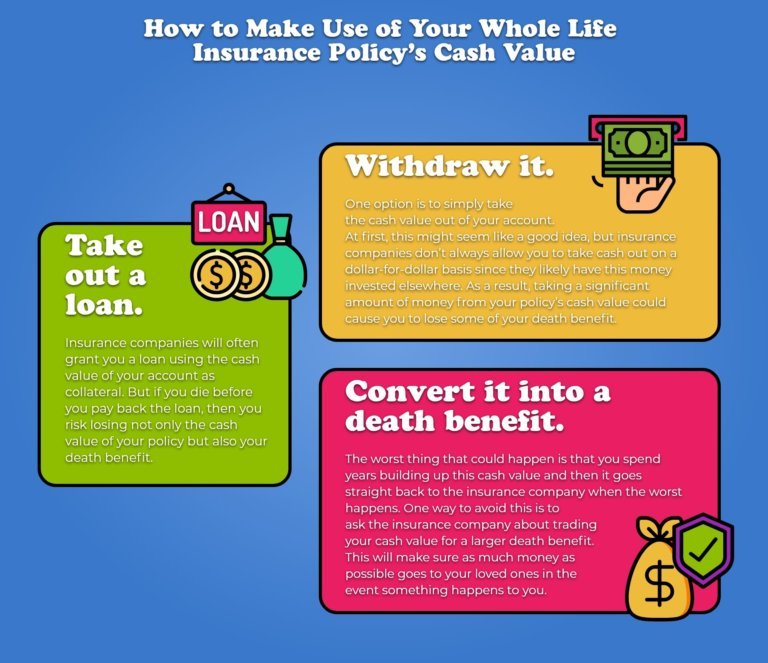

With whole life insurance policies, though, eventually you will be covered, yet you will keep paying premiums. This “extra” money is then deposited into a savings account, and your life insurance policy will begin to accumulate cash value. But when you die, if you’ve done nothing with this cash value, then the insurance company will pay out your death benefit and absorb the account’s cash value.

To prevent this from happening, there are a few things you can do when your account begins to accumulate significant cash value:

Other options require you to get a specific type of whole life insurance policy, such as:

Universal Whole Life

Universal whole life policies allow you to start paying for your insurance premiums using the accounts cash value after your account has been “paid up,” meaning the cash value of your account exceeds the cost to insure you (i.e. the death benefit that would need to be paid up should you pass away.) But if you do this, you just need to be careful that you don’t blow through the policy’s cash value too quickly, as this could cause your policy to lapse.

These types of whole life insurance policies also allow you to add to your death benefit, provided you pass a medical examination. In this sense, universal whole life insurance is considered to be quite a bit more flexible than traditional whole life insurance. But this comes with a bigger price tag.

Variable Whole Life

Variable whole life gives you more autonomous control over how your premiums are invested. Essentially, you will be free to invest them in stocks, bonds, mutual funds, and any other investment vehicles you see fit.

The advantage of this is that you can grow the cash value of your account much more quickly than you might with a traditional policy, but the disadvantage is the considerable risk you are assuming by putting your life insurance into the stock market. Should the account not perform well, then the cash value of the account and the death benefit will decrease.

Variable-Universal Whole Life Insurance

This is essentially a combination of these two policy types. You have the freedom to invest your premiums as you want, and you can also adjust your policy after it has been “paid up.” But because of all this extra control, premiums tend to be higher for variable-universal whole life insurance.

Factors Affecting Your Life Insurance Costs

The type of insurance policy you buy is one of the biggest factors determining the price of your life insurance premiums. In general, term insurance is cheaper because it presents less of a risk to the insurance company.

For example, if a 30-year-old healthy female buys a 15-year term policy, the insurance company is taking less risk than if they insure a 50-year-old make for life. Chances are the 30-year-old female will outlive the term, meaning the insurance company made money. But for the 50-year-old male, there’s a good amount of risk that the insurance company won’t be able to grow his account fast enough to cover the death benefit, so, in response, they need to charge higher premiums.

In this example, however, it’s clear there are other factors at play, which we will discuss in more detail.

Death Benefit

The size of your death benefit is going to have a huge impact on how much you pay in life insurance premiums. In short, the bigger the benefit, the more you will need to pay. Here’s a breakdown of average prices based on some common death benefit figures for whole life insurance policies for healthy people aged 30-50:

However, if you opt for term life insurance instead of whole life, you can get similar benefits for considerably less. The average price for a $500,000 term life insurance policy is just $169/month.

Term

Another thing that will impact your premiums is the length of your term. As we’ve discussed, whole life insurance is more expensive, and longer-term policies are also more expensive because they are riskier for insurance companies.

Age and Gender

Age is something that does not have to do with the type of policy you choose but that will have a dramatic impact on how much you pay for life insurance. This is because, quite simply, the older you are, the higher your risk of death. And since life insurance companies are looking to not have to pay, they don’t want to insure someone for twenty years who is already 55, unless you’re willing to bear most of that risk yourself in the form of higher premiums.

Gender also affects how much you will pay for life insurance because women have a higher life expectancy than men (81.1 years as compared to 76.1), and this means insurance companies will charge less to insure them.

To give you an idea of how much age and gender affect the cost of your insurance premiums, consider the differences in price for a $500,000, 20-year term life insurance policy for men and women from different age brackets. As you can see, purchasing this type of policy at age 50 will cost you three times as much as it cost when you were 30, and for a man, things get even more expensive as you get older.

Health

Your health is also something that is going to impact how much you pay. Logically, people in good health are charged less than those with a serious medical condition. Expect to have to go through a medical exam at some point in the process of buying life insurance.

Insurance companies will also take into account your family’s medical history. They will be looking for things such as heart disease, cancer, diabetes, addiction, etc., and if there is a strong history of something in your family, you can expect to pay more.

Tobacco Use

Smoking poses a tremendous threat to your health and well-being, which is why insurance companies will charge smokers more than non-smokers. They typically find out if you are a smoker from your doctor, but know that you can ditch this label if you quit smoking and get a doctor to corroborate that you’re no longer using tobacco.

Here are some sample prices for a $250,000, 20-year term for women smokers:

When you compare these to the numbers above for a $500,000 policy, it becomes clear how much smoking affects your life insurance premiums. At age 30, you will essentially be paying half the price as a non-smoker, and by age 50, you are paying about four or five times as much as those who don’t smoke.

Credit History

Insurance companies obviously want to know they are going into business with someone who can pay their bills. As a result, expect them to run a credit report during the quoting process, and don’t be surprised if they try to charge you more because you have bad credit.

Hobbies, Lifestyle, Occupation

In their attempt to assess how much risk you pose to the company, life insurance companies will want to know what kind of life you live. If you work a quiet job and don’t engage in high-risk behavior, you will probably be charged less. But if you’re an adrenaline junky who goes BASE jumping on the weekends and works as a fire-breather, don’t be surprised if you’re asked to pay higher premiums.

How to Save on Your Life Insurance

Now that you’ve seen what goes into determining the cost of your life insurance, you might be wondering what you can do to save. Obviously, some things you can’t change, such as your age or your gender, but there are some steps you can take to save, such as:

Choose Term over Whole Life Insurance

Whole life insurance seems to be the more appealing option because it covers you for your “whole” life. But in most cases, this is more coverage than you need. By the time you’re sixty or seventy, you hope your children are well-established and will be able to manage without you, so there’s no need to keep paying those high premiums. Instead, it’s better to get a term policy that covers you for the years when your children would not be able to take care of themselves.

Of course, the savings account part of whole life insurance is nice, but there are other ways for you to put money aside that are going to be more lucrative, and then you can leave that as an inheritance. This strategy will save you money in the short- and long-term since you will pay less in premiums.

Shop Around

When looking for life insurance, make sure to get quotes from at least three if not more different companies. Everyone has their own method for assessing risk, and you might be able to save a good bit by going with one company over another.

If you already have insurance, especially term insurance, keep an eye out for new offers. You may be able to switch companies and save when your policy expires.

Adopt Healthier Lifestyles

As mentioned, your health has a huge impact on how much you will pay in health insurance premiums. So, if you feel as though you are paying too much, or if life insurance is out of reach because of your health, then it might be time to try and make a change.

This is easier said than done, but changing your diet and exercise habits, or quitting smoking, can have a tremendous impact on your health, and insurance companies will reward you with lower premiums.

Constantly Reevaluate Your Death Benefit

When most people first buy life insurance, they do it thinking of the worst. For example, a young couple with young children is going to be thinking about what will happen if both parents die in the next year, and this will motivate them to buy a larger insurance policy with a bigger death benefit.

This is good logic at the time of purchase, but fifteen years later when the kids have grown and your financial situation is much more secure, that $1 million policy might be overkill, yet you’re still paying for it. However, you can speak to your insurance company about lowering your death benefit in exchange for lower premiums. Do this constantly to ensure you’re not paying for something you don’t really need.

Conclusion

Determining the overall average cost of life insurance is difficult to do because of the many different factors that determine premiums and also because of the many different options available. However, we hope that by going over these different options and the factors that affect them, you now better understand life insurance.

Now, it’s time to put this information to work and shop around for an insurance policy that fits your budget and offers you the comfort, security, and peace of mind that life insurance was designed to provide.

https://www.carefulcents.com/the-average-cost-of-life-insurance/?msID=f84c654e-68bc-4bf4-af04-58456e04289d