Global foreign direct investment (FDI) flows are expected to bottom out in 2021 and recover some lost ground with an increase of 10% to 15%, according to UNCTAD’s World Investment Report 2021, published on 21 June.

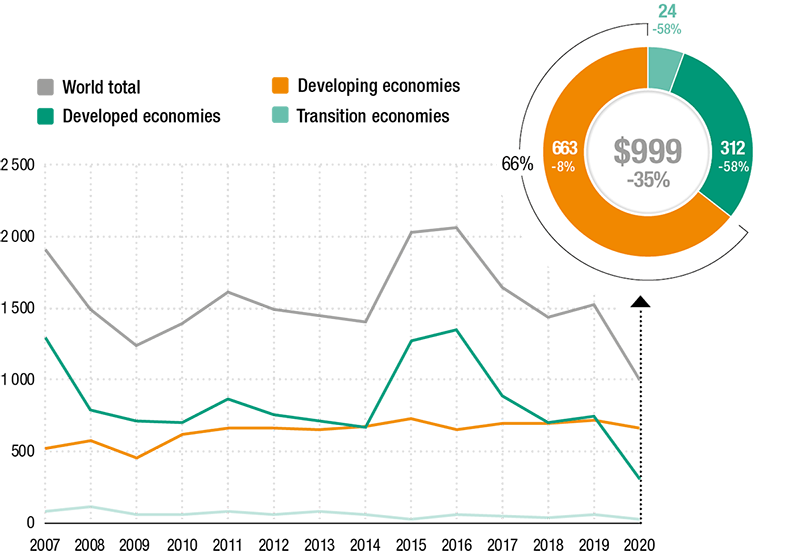

FDI flows plunged globally by 35% in 2020, to $1 trillion from $1.5 trillion the previous year, the report says. Lockdowns caused by the COVID-19 pandemic around the world slowed down existing investment projects, and the prospects of a recession led multinational enterprises (MNEs) to reassess new projects.

The fall was heavily skewed towards developed economies, where FDI fell by 58%, in part due to corporate restructuring and intrafirm financial flows.

FDI in developing economies was relatively resilient, declining by 8%, mainly because of robust flows in Asia. As a result, developing economies accounted for two thirds of global FDI, up from just under half in 2019 (Figure 1).

Figure 1 – Foreign direct investment inflows, global and by group of economies, 2007–2020

(Billions of dollars and per cent)

Source: UNCTAD, World Investment Report 2021.

Source: UNCTAD, World Investment Report 2021.

“These investment types are crucial for productive capacity and infrastructure development and thus for sustainable recovery prospects,” Acting UNCTAD Secretary-General Isabelle Durant said.

Sectors vital for development hit hard

COVID-19 has also caused a collapse in investment flows to sectors relevant for the Sustainable Development Goals (SDGs) in developing countries (Table 1).

Table 1 – The impact of COVID-19 on

international private investment in SDGs

Source: UNCTAD, World Investment Report 2021.

Source: UNCTAD, World Investment Report 2021.Note: Percentage changes represent aggregate growth trends of project finance and greenfield investment values for the period 2019-2020.

All but one SDG investment sectors registered a double-digit decline from pre-COVID-19 levels. The shock exacerbated declines in sectors that were already weak before the pandemic – such as power, food and agriculture, and health.

“The drop in foreign investment in SDG-related sectors may reverse the progress achieved in SDG investment in recent years, posing a risk to delivering the 2030 Agenda for Sustainable Development and to sustained post-pandemic recovery,” Ms. Durant said.

Regional trends

FDI trends in 2020 varied significantly by region. In developing regions and transition economies they were relatively more affected by the impact of the pandemic on investment in global value chain-intensive and resource-based activities. Asymmetries in fiscal space for the roll-out of economic support measures also drove regional differences.

FDI flows to Europe declined by 80% while those to North America fell less sharply (-40%). The fall in FDI flows across developing regions was uneven, with 45% in Latin America and the Caribbean, and 16% in Africa.

In contrast, flows to Asia rose by 4%, with East Asia being the largest host region, accounting for half of global FDI in 2020. FDI to transition economies declined by 58%.

The pandemic further deteriorated FDI in structurally weak and vulnerable economies. Although inflows in least developed countries (LDCs) remained stable, greenfield announcements fell by half and international project finance deals by one third. FDI flows to small island developing states (SIDS) fell by 40%, and those to landlocked developing countries (LLDCs) by 31%.

MNEs, the key actors in global FDI, are weathering the storm. Despite the 2020 fall in earnings, the top 100 MNEs significantly increased cash holdings, attesting to the resilience of the largest companies. The number of state-owned MNEs, at about 1,600 worldwide, increased by 7% in 2020, with some new entrants resulting from equity participations as part of rescue programmes.

Bottoming out likely in 2021

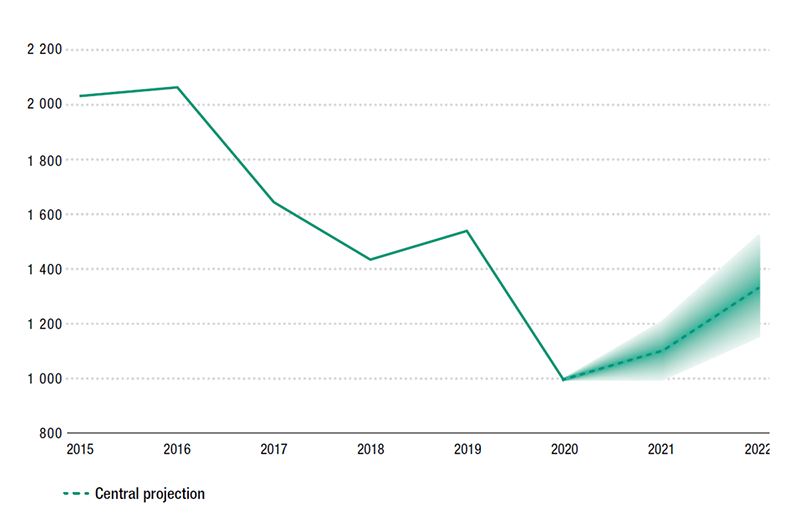

Looking ahead, global FDI flows are expected to bottom out in 2021 and recover some lost ground with an increase of 10% to 15% (Figure 2). “This would still leave FDI some 25% below the 2019 level. Current forecasts show a further increase in 2022 which, at the upper bound of projections, bring FDI back to the 2019 level,” said UNCTAD’s director of investment and enterprise, James Zhan.

Figure 2 – Foreign direct investment outflows, top 20 home economies, 2017 and 2018

(Billions of dollars)

Source: UNCTAD, World Investment Report 2021.

Source: UNCTAD, World Investment Report 2021.

Prospects are highly uncertain and will depend on, among other factors, the pace of economic recovery and the possibility of pandemic relapses, the potential impact of recovery spending packages on FDI, and policy pressures.

The relatively modest recovery in global FDI projected for 2021 reflects lingering uncertainty about access to vaccines, the emergence of virus mutations and the reopening of economic sectors.

“Increased expenditures on both fixed assets and intangibles will not translate directly into a rapid FDI rebound, as confirmed by the sharp contrast between rosy forecasts for capex and still-depressed greenfield project announcements,” Mr. Zhan said.

The FDI recovery will be uneven. Developed economies are expected to drive global growth in FDI, both because of strong cross-border mergers and acquisitions (M&A) activity and large-scale public investment support.

FDI inflows to Asia will remain resilient as the region has stood out as an attractive destination for international investment throughout the pandemic. A substantial recovery of FDI to Africa and to Latin America and the Caribbean is unlikely in the near term.

African Eye Report