-

Globalisation is being rewired by geopolitics and policy shifts. The financial system will have to adapt to better serve the real economy’s needs.

-

Policy volatility is now a persistent challenge for trade, investment and development.

-

Financial shocks spill over rapidly into the real economy, revealing gaps in the global economic architecture.

-

Developing economies drive global growth but face the highest financing and climate risks.

-

Coordinated reforms linking trade, finance, debt and climate action can restore stability and recenter development.

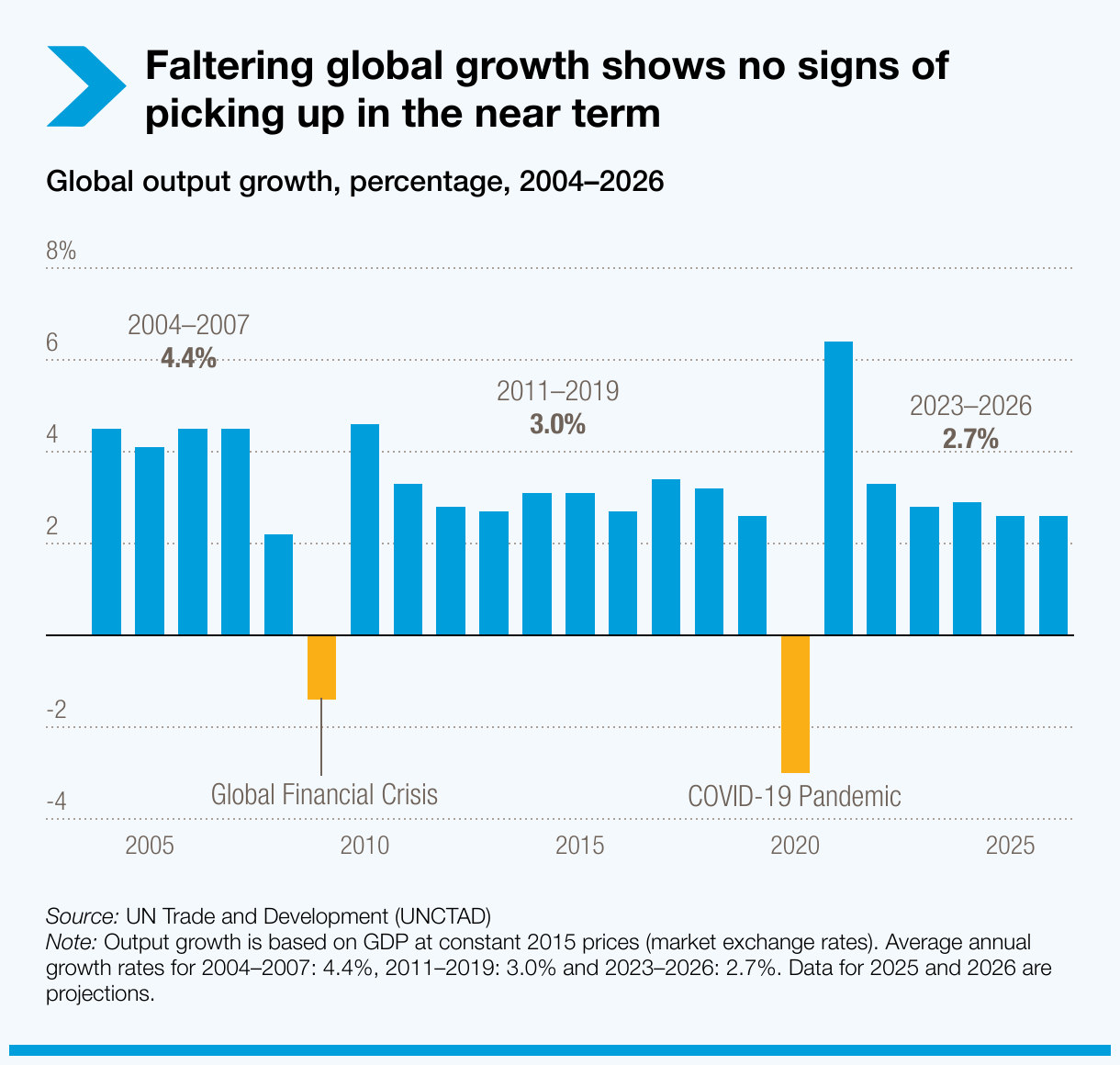

Global growth will slow to 2.6% in 2025, down from 2.9% in 2024, as global trade and investment face growing pressure from financial volatility and geopolitical uncertainty, according to UN Trade and Development’s new “Trade and Development Report 2025: On the Brink – Trade, finance and the reshaping of the global economy”.

The report shows that shifts in financial markets move global trade almost as strongly as real economic activity, influencing development prospects worldwide.

Global growth shows no signs of picking up

Global output growth, percentage, 2004–2026

4.4%

3.0%

2.7%

{kind=link}

UN Trade and Development (UNCTAD) Secretary-General Rebeca Grynspan said the findings show how financial conditions increasingly determine the direction of global trade: “Trade is not just a chain of suppliers. It is also a chain of credit lines, payment systems, currency markets and capital flows.”

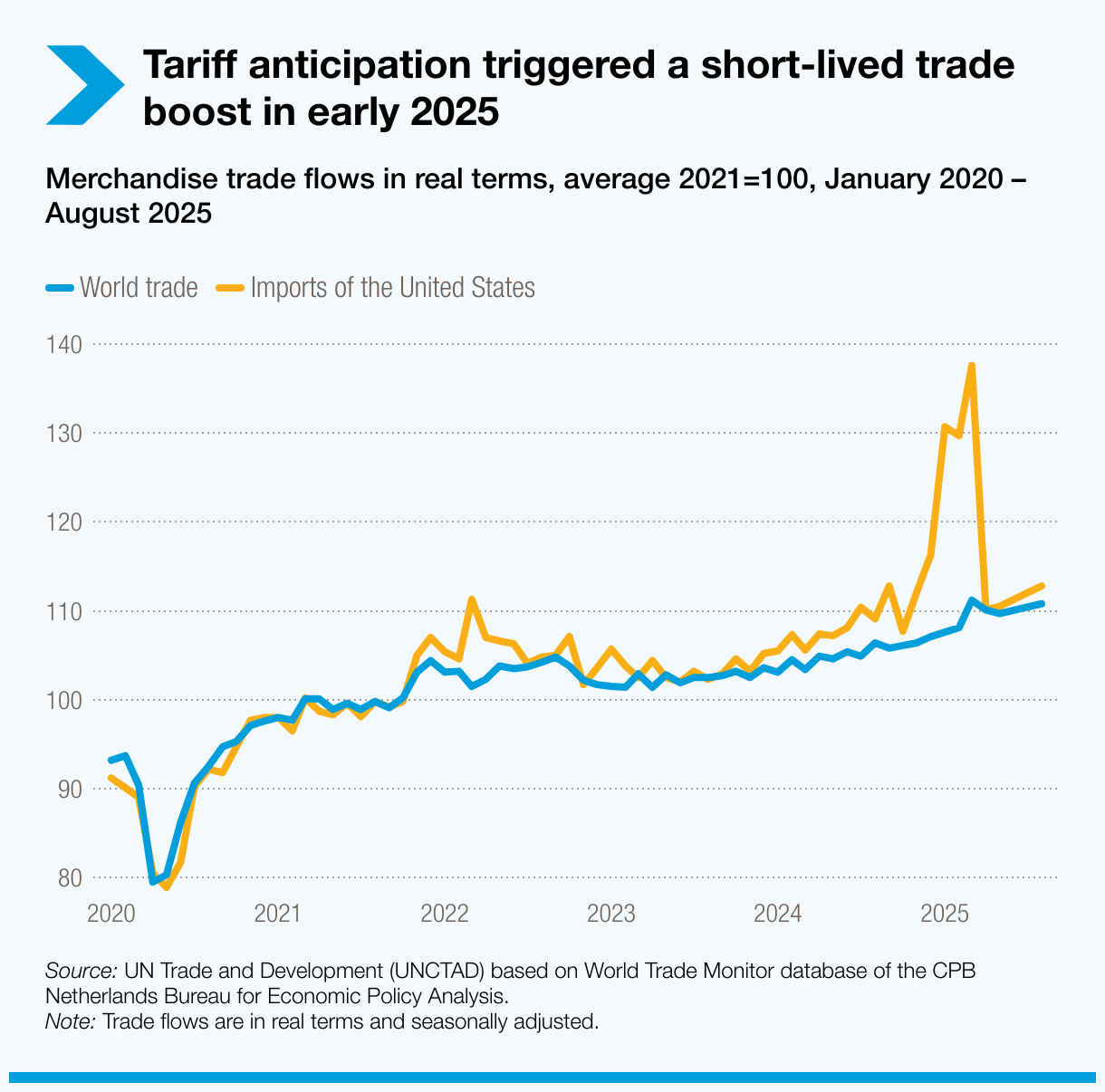

Global trade rose by about 4% early in 2025, driven in part by firms accelerating imports ahead of tariff changes, but also by structural shifts: Services are expanding faster, supported by growth in the digital economy and artificial intelligence, and South–South trade is growing above average.

Tariff anticipation triggered a short-lived trade boost in early 2025

Merchandise trade flows in real terms, average 2021=100, January 2020 – August 2025

{kind=link}

Beneath these factors, underlying trade growth is estimated at between 2.5% and 3% and is expected to ease further as financial conditions influence production and investment decisions more strongly.

More than 90% of global trade depends on bank finance. Dollar liquidity and cross-border payment systems are also crucial for international trading activities. This deep reliance on financial channels makes trade closely linked to global financial and monetary conditions. A shift in interest rates or investor sentiment in a major financial centre can affect trade volumes worldwide. For developing countries, where access to affordable credit is limited, these financial pressures can undermine otherwise viable trade transactions.

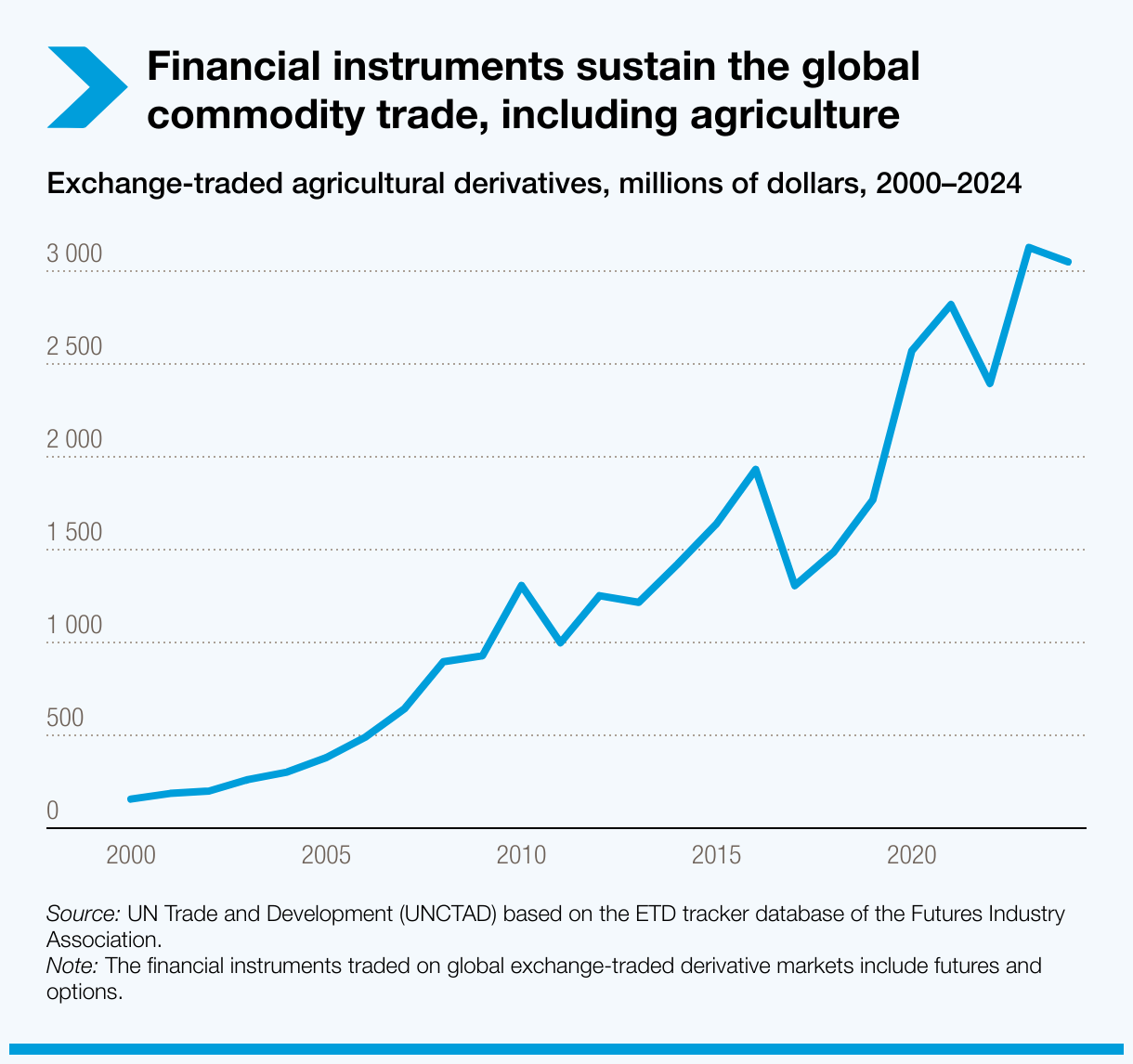

The report also highlights the increasing role of financial factors of commodity markets, particularly in essential food systems.

Financial instruments power global commodity trade, including agriculture

Exchange-traded agricultural derivatives, millions of dollars, 2000–2024

{kind=link}

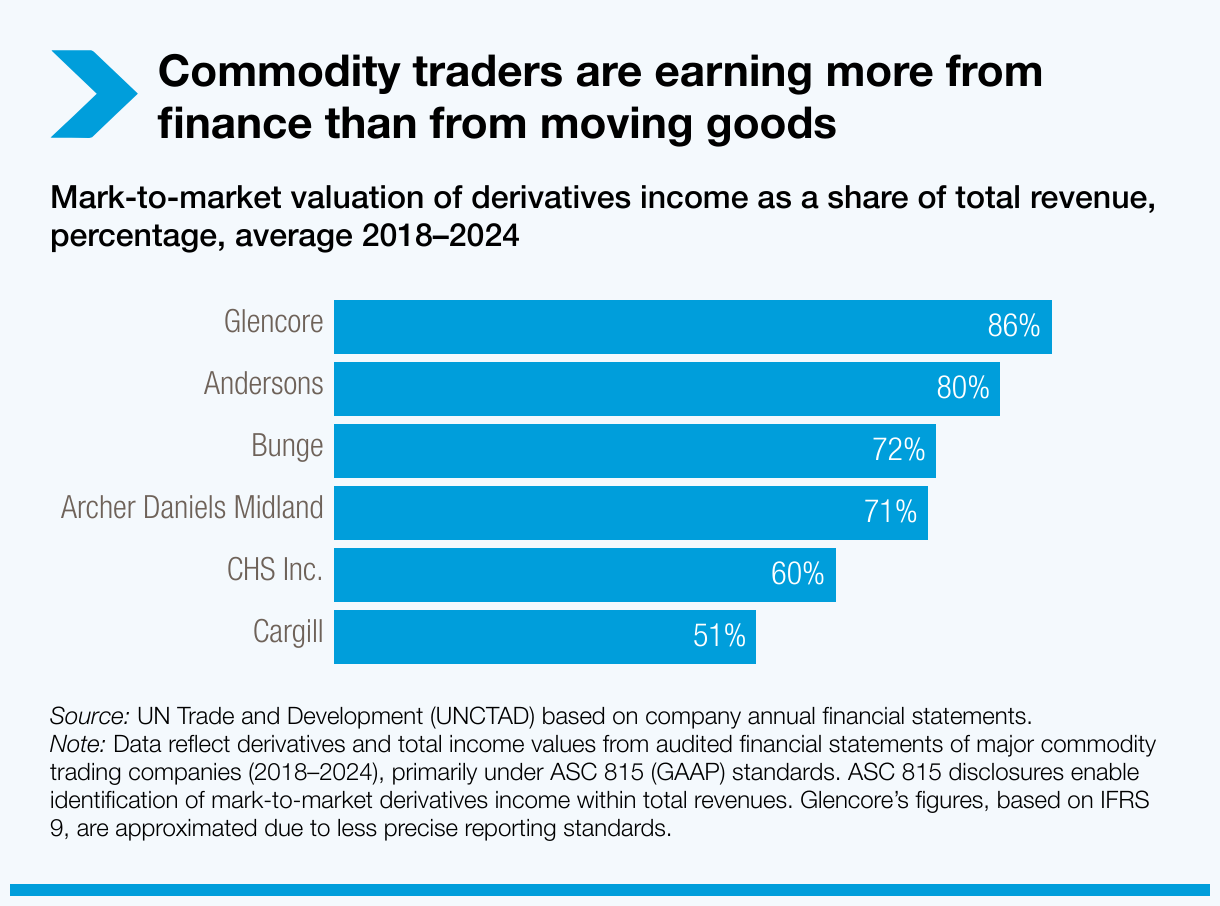

For several major food trading companies, more than 75% of income now stems from financial operations rather than the physical movement of goods.

Commodity traders now earn more from finance than from moving goods

Mark-to-market valuation of derivatives income as a share of total revenue, percentage, average 2018–2024

{kind=link}

Developing economies face mounting pressures

Developing economies are forecast to grow by 4.3%, significantly faster than advanced economies. But they face higher financing costs, greater exposure to sudden shifts in capital flows and rising climate-related financial risks. These factors limit the fiscal and investment space needed to sustain growth.

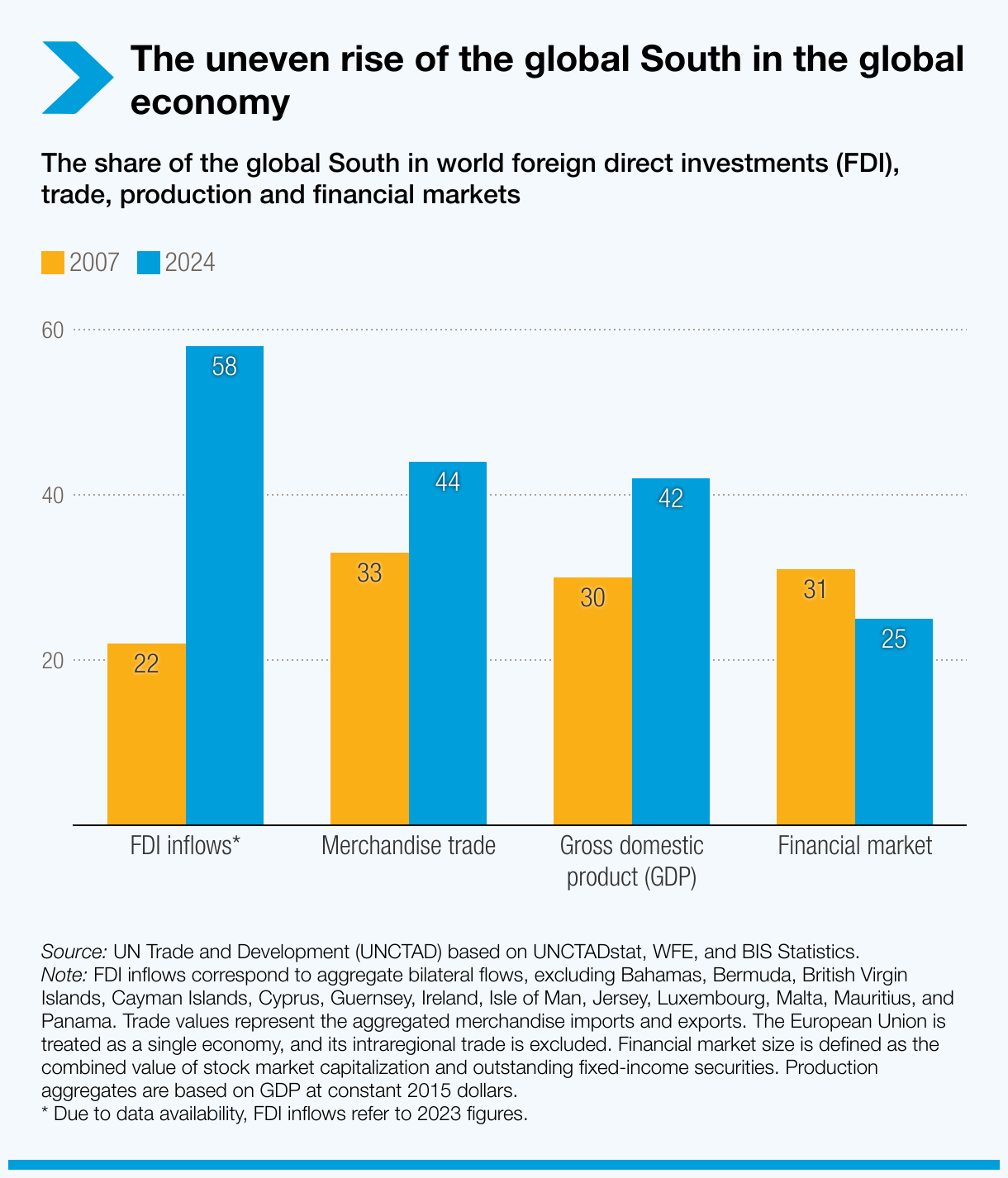

The global South accounts for more than 40% of world output, nearly half of global merchandise trade and more than half of global investment inflows.

The uneven rise of the global South in the global economy

The share of the global South in world foreign direct investments (FDI), trade, production and financial markets

204060

{kind=link}

Yet its role in global financial markets remains limited. Excluding China, developing countries represent only about 12% of global equity market value and around 6% of global bond issuance.

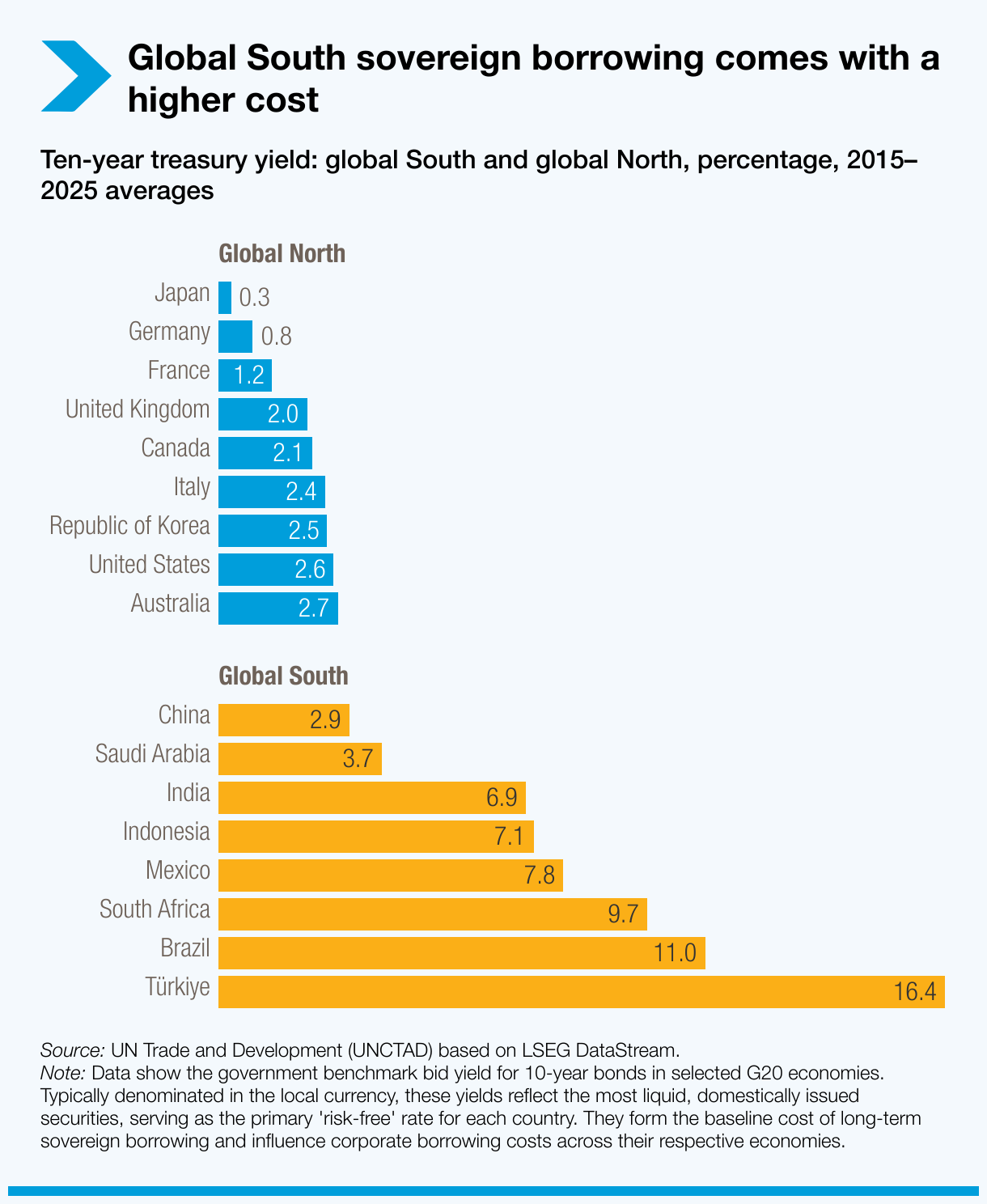

Because their domestic financial markets are small, many developing economies rely on external borrowing at significantly higher cost. Borrowing rates of 7% to 11% are common, compared with 1% to 4% in major advanced economies.

Borrowing costs are higher for the global South

Ten-year treasury yield: global South and global North, percentage, 2015–2025 averages

{kind=link}

These elevated costs often reflect structural issues in the international financial architecture rather than economic fundamentals, reducing long-term investment and slowing growth.

Climate vulnerability adds to financial pressures. Countries repeatedly exposed to extreme weather now pay an estimated 20 billion dollars more each year in interest because lenders perceive them as riskier. Since 2006, these additional premiums have cost climate-vulnerable economies about 212 billion dollars – resources that could have supported social investment or climate adaptation.

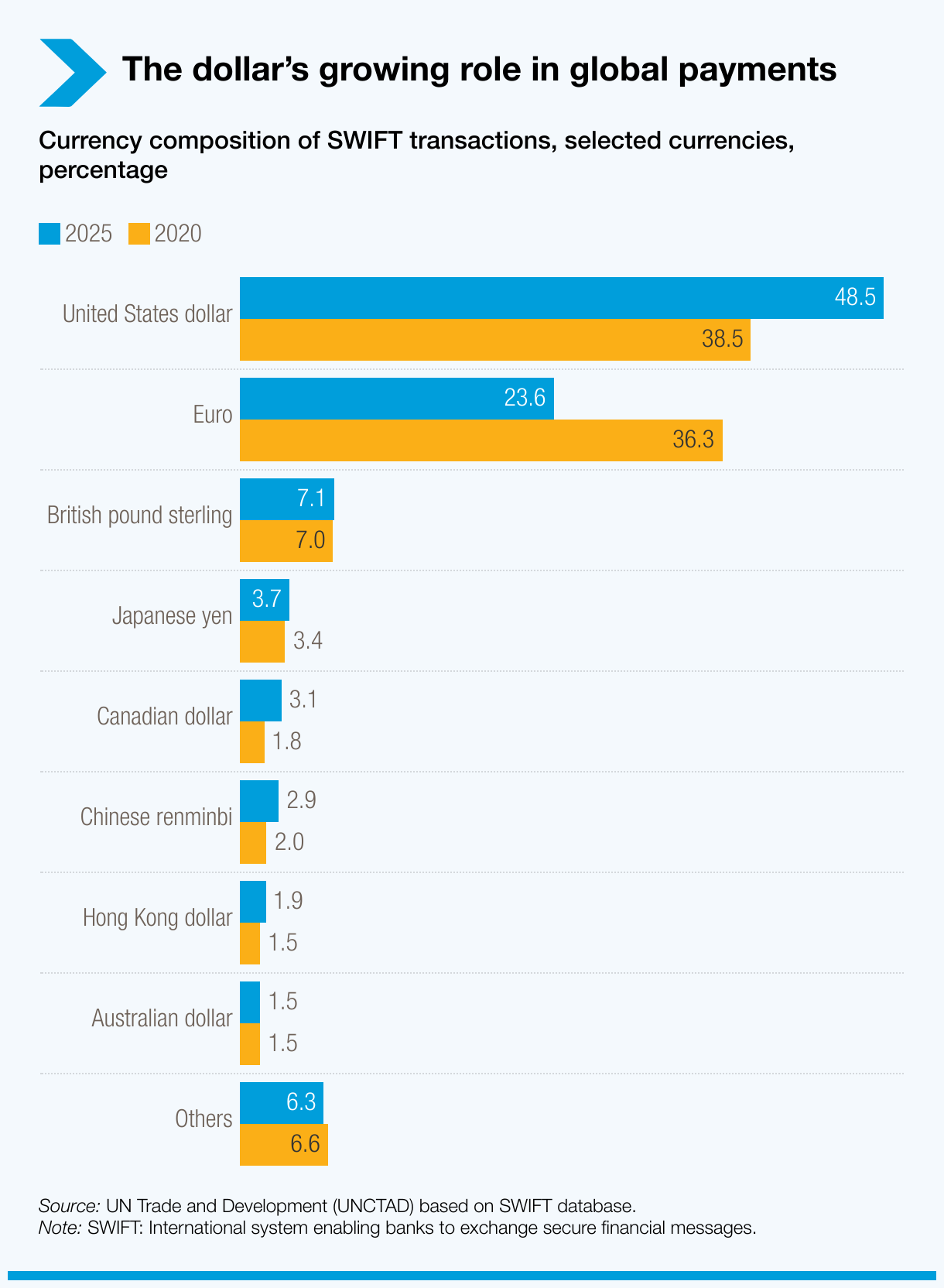

Dollar dominance continues to anchor global finance

Despite gradual diversification of international reserves, the dollar remains central to global finance. Its share of international payments through SWIFT has risen from 39% to about 50% in five years.

The dollar’s growing role in global payments

Currency composition of SWIFT transactions, selected currencies, percentage

{kind=link}

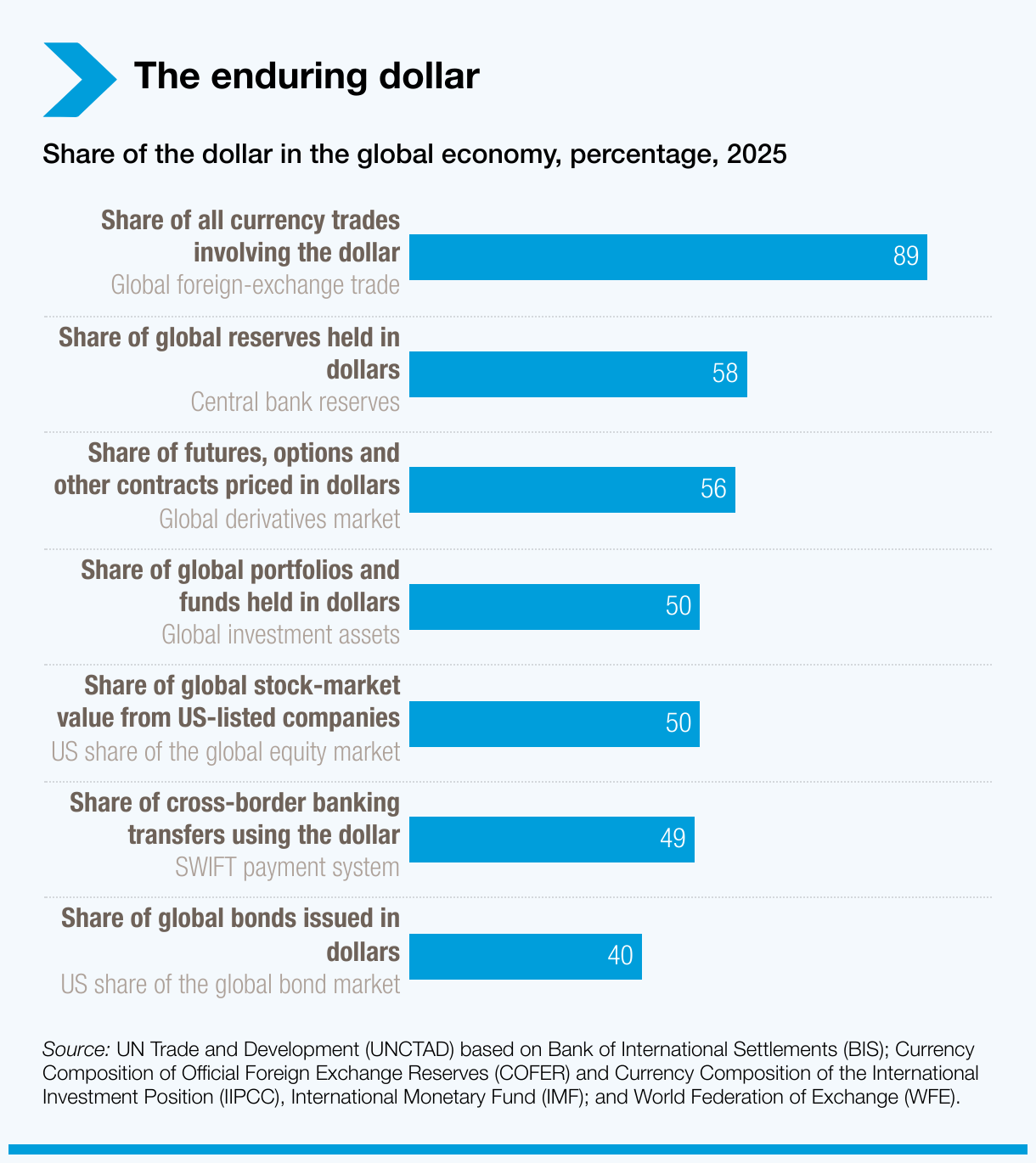

The United States also accounts for half of global equity market value and about 40% of global bond issuance.

The enduring dollar

Share of the dollar in the global economy, percentage, 2025

{kind=link}

While this provides stability in uncertain periods, it also links developing economies to financial cycles over which they have limited influence.

Targeted reforms to restore stability and support development

UNCTAD outlines a set of practical reforms aimed at reducing financial vulnerability, improving predictability and supporting stronger alignment between trade, finance and development. The report calls for:

- Fix the multilateral trade dispute system so rules are enforced and uncertainty is reduced.

- Update trade rules for today’s economy; including services, digital trade, climate action and new industrial strategies.

- Close data gaps on trade and investment statistics to better inform and coordinate policies.

- Reform the international monetary system to limit harmful swings in currencies and capital flows.

- Strengthen regional and domestic capital markets so developing countries can raise affordable long-term finance.

- Use macroprudential tools (rules that reduce negative financial spillovers) to better protect trade and investment.

- Improve transparency in commodity trading and expand access to affordable trade finance, especially for small businesses.

Rebeca Grynspan said reconnecting trade and finance is essential for lasting stability: “What does genuine resilience require? Integrated policy frameworks that recognize links between trade, finance and sustainability.” She added that coordinated reforms can strengthen long-term development prospects: “Fundamentally, we cannot understand trade isolated from finance.”