Latest analysis released by Partech Ventures, a leading venture capital firm specializing in information and communication technologies, has revealed that Venture Capital (VC) funding raised by African tech start-ups in 2017 totaled US$ 560 million, compared to US$ 366.8 Million in 2016.

This represents a 53% plus growth year-on-year (YoY).

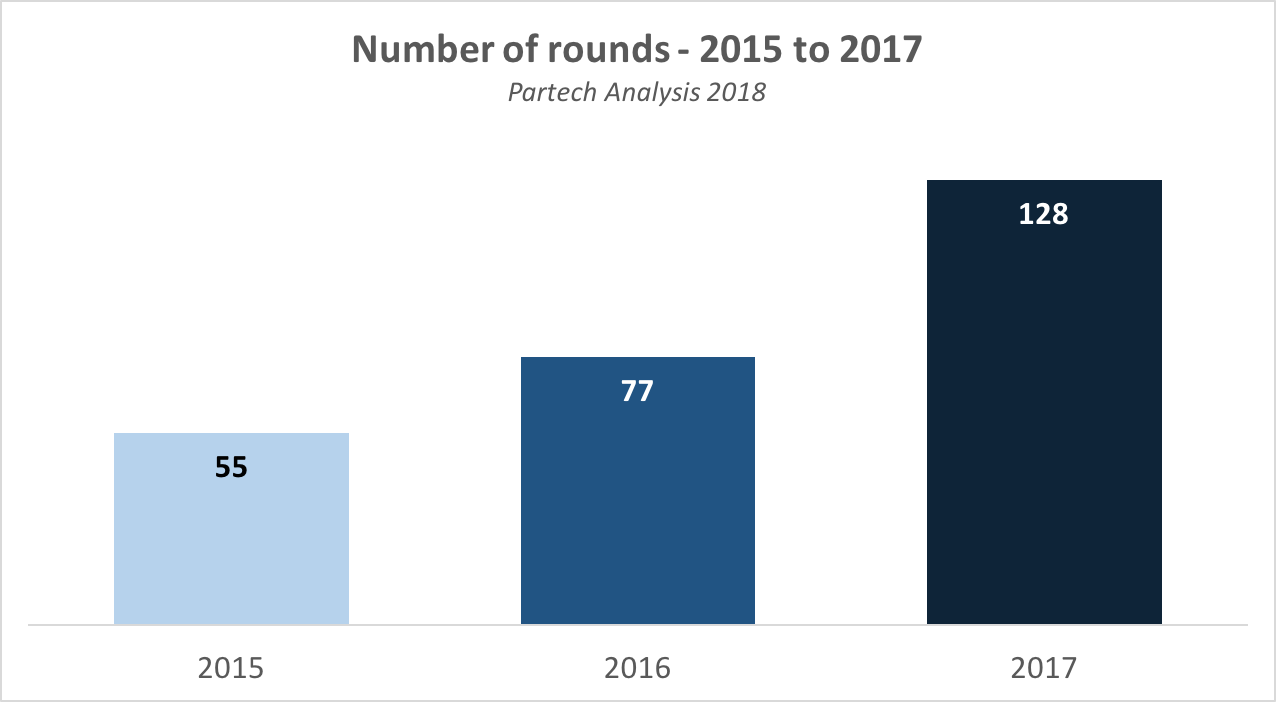

This shows that African tech scene has definitively turned another corner this year with increasing venture capital commitments to African start-ups towards a larger number of transactions, 128 in total, and a broader geographic distribution.

“Africa is not just grabbing the world’s attention: African entrepreneurs are leveraging tech & digital to tackle the continent’s fundamental challenges, they are the leading innovators in key verticals, leapfrogging usages, and Venture Capital has become the core catalyst to these opportunities”, according to the analysis.

Findings

124 African tech start-ups raised a total of US$ 560 Million in equity through 128 rounds.

1) The VC funding raised by African tech start-ups in 2017 totalled US$ 560 Million, compared to US$ 366.8 Million in 2016, a +53% growth YoY.

- This is a x14 growth multiple since 2012 in terms of amount invested.

- If you exclude Off-grid deals, investment in digital start-ups in Africa have actually almost doubled, +90%, with US$ 440 Million in 2017 vs. US$ 231 Million in 2016.

2) The ongoing transformation of the VC tech space translates in the number of start-ups that were funded. In 2017, it has jumped to a total of 128 rounds (Seed+ to Growth stages) from 124 African tech start-ups, compared to 77 rounds last year from 74 start-ups; a +61% growth YoY in the number of VC-backed tech start-ups.

The Top 3 markets, South Africa, Kenya and Nigeria, absorbed 76% of the total funding, down from 81% in 2016.

The geographic distribution remains predominantly focused on the top 3 markets with an investment landscape that smoothly continues to expand.

1) Regarding amounts raised, the leading trio is unchanged, however:

- South Africa is taking the top spot with US$ 168 Million in funding (30% of total investment), showing a +74% growth YoY largely due to the Takelot deal.

- Kenya is truly confirming its leading tech start-up nation role with US$ 147 Million(26% of total), showing a strong +58% growth YoY.

- Nigeria has slowed down compared to its 2 challengers, with US$ 115 Million (20% of total), representing a +5% growth YoY.

2) South Africa is yet again #1 in number of start-ups getting funded with 42 deals (33% of total transaction), followed by Kenya with 25 deals (20% of total) and Nigeria with 17 deals (14% of total).

3) Egypt is seriously stepping up, ranked #4, both in terms of total investments and transactions, with notably a number of deals close to Nigeria, 14 vs.17 i.e. 12% of the total transactions.

4) Francophone African countries are confirming traction, now representing almost 14% of the total transactions (16 deals) and 10% of the total funding (US$ 55.5 Million) with 5 countries: Rwanda, Senegal, Morocco, Cameroun and Tunisia.

The Top 3 verticals remain Off-Grid Tech, Fintech & E/M/S-Commerce, attracting 61% of the total funding, down from 72% in 2016.

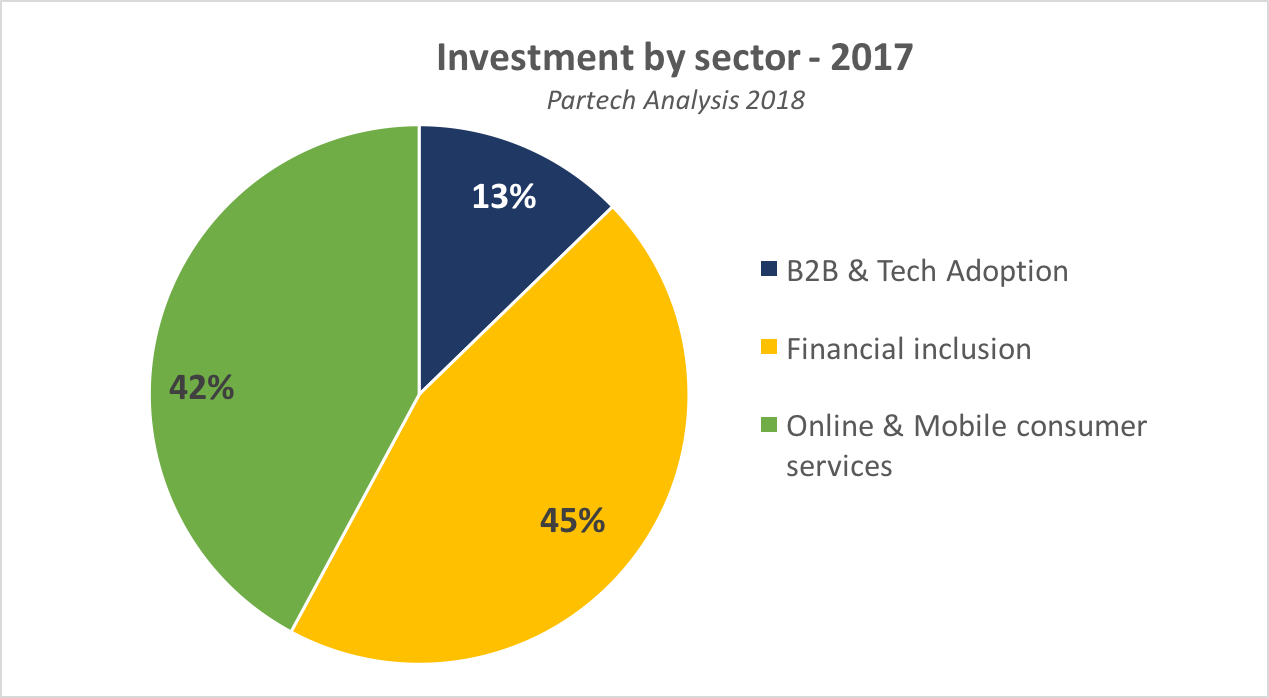

Two sectors, Financial Inclusion and Online & Mobile Consumer Services, represent 87% of total funding thanks to the Top 3 verticals that remain Off-Grid Tech (#1), Fintech (#2) and E/M/S-Commerce (#3).

However, the sector distribution sees B2B & Tech Adoption showing a steep increase to 13% of total funding (compared to 3.3% in 2016) driven by the B2B/Enterprise vertical representing this year 18% of the total deals.

1) Financial Inclusion accounted this year for 45% of the total investment at US$ 253 Million, down from 56% in 2016 across 46 transactions.

- Off-Grid Tech – US$120M (-10% YoY), 21% of total funding, 13 deals. As a good sign of market maturity, Off-Grid tech start-ups raised almost the same amount of equity in 2017 (US$ 134 Million in 2016) but additionally deeply leveraged debt financing for growth capital with (information outside the scope of this report) another US$ 117 Million raised in debt.

- Fintech – US$119M (+70% YoY), 21% of total funding, 29 deals.

- InsurTech – US$14M (+470% YoY), 2.5% of total funding, 4 deals.

2) Online & Mobile Consumer Services accounted for 42% at US$ 236 Million, stable compared to last year’s 40,5% share, across 54 transactions. The 4 main sub-verticals this year are:

- E/M/S-Commerce – US$105M (+74% YoY), 19% of funding, 19 deals.

- EdTech – US$65M (+120% YoY), 12% of total funding, 5 deals.

- Personal Services – US$41M (+3000% YoY), 7% of total funding, 16 deals.

- HealthTech – US$21M (+125% YoY), 4% of total funding, 7 deals.

3) B2B & Tech Adoption accounted for 13% at US$ 71 Million, compared to 3,3% last year, across 20 transactions. This spectacular trend goes mainly to Enterprise Software start-ups.

- Enterprise – US$60M (+800% YoY), 11% of total funding, 23 deals.

- Connectivity – US$10M (+360% YoY), 2% of total funding, 3 deals.

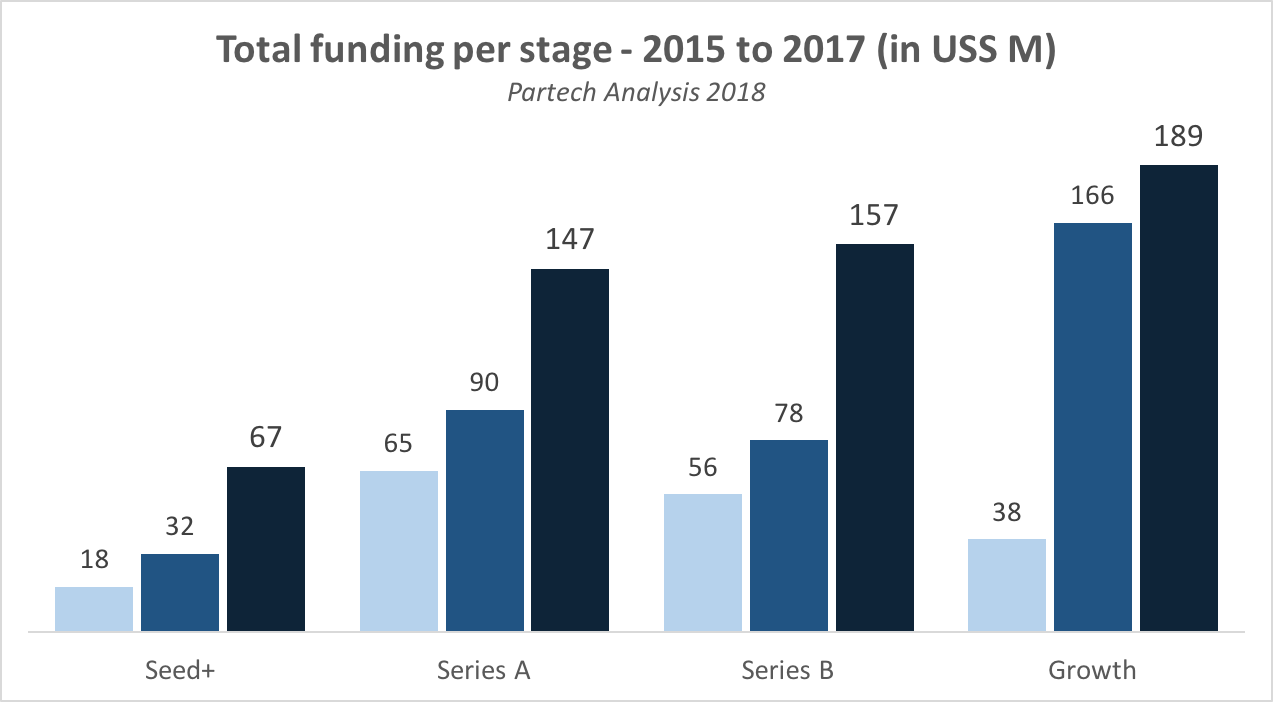

Africa’s Series A deal size reached US$ 4.5 Million in 2017

Fund managers are focusing more and more on tech start-ups. 2017 is the year where the private equity sector mindset is moving to a long-term strategy where access to growth/PE capital requirement to build game-changing African SMBs requires better structuring of early-stage equity funding in the first place.

1) Total funding going to Seed+ and Early Stage (Series A & Series B) has grown +86% YoY to reach US$ 371 Million in 2017.

2) Seed+ round size was US$0.91M (vs. US$ 0.83m in 2016) with 73 transactions, +92% YoY in number of transactions.

3) Series A round size has reached US$4.5M in 2017 (vs. US$ 3.7m in 2016) with 33 transactions, +38% YoY in number of transactions.

4) Series B is stabilizing at US$10.5M (vs. US$ 11.1m in 2016) with 15 transactions, +114% YoY in number of transactions.

Methodology

Our methodology remains unchanged. We do track data limited to certain types of African deals and start-ups. As a recap:

1) The numbers only include deals higher than US$200K and voluntary exclude what we call megadeals i.e. above US$ 100 Million (this year the largest round accounted for was Takelot $69M Series D).

2) The numbers exclude any Grant, Debt and ICO deals.

3) The numbers englobe African start-ups that we define as the ones having their primary market in Africa (i.e. in terms of operation & revenues). It is independent of HQs location or country of incorporation.

4) For start-ups with a local presence in more than one African country, only one primary country of operation has been identified and that is where the investment is accounted for.

African Eye Report