Lagos, Nigeria, February 13, 2019// – Analysts have presented different possibilities for the Nigerian economy after the February and March elections, with most of them saying that a change in political leadership would most likely inspire hope and engender economic growth.

A consensus of opinions from research notes by investment houses and experts on economic growth suggest that elections do affect gross domestic growth (GDP), inflation, and exchange rates, especially when they are credible, transparent, and when power moves into the hands of the opposition.

At a breakfast meeting organised by NASD Plc recently, Bola Ajomale, CEO of NASD Plc, noted that a lot would depend on the outcome of the election, that a successful election would mean the outlook for 2019 would be very bright for the business community and investors.

He said if there is quick resolution of the issues arising from the poll, the country would continue as normal, adding that if there is no quick resolution there would be trouble.

Doyin Salami, an economist at the event, said Nigeria should expect a tighter monetary policy if the incumbent wins, and this would likely see current exchange rates as well as interest rates maintained at the level they were at least for the first half of 2019.

On the other hand, Salami noted that this could change if the main opposition defeats the incumbent.

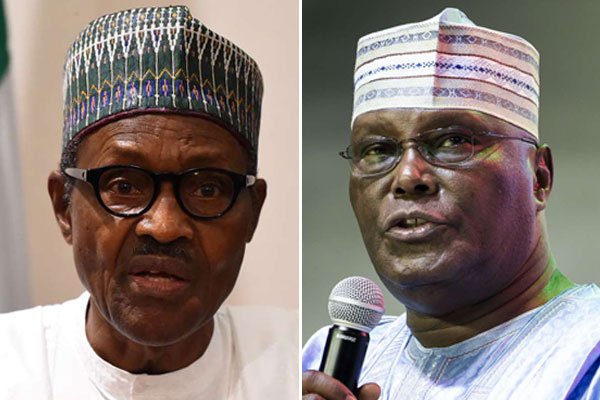

In a presentation to the Harvard Business School Association, Bismarck Rewane, chief executive officer of Financial Derivatives Company (FDC), Nigeria’s foremost research firm, noted in late January that growth would remain tepid and sub-optimal owing to a lull in business activities if the incumbent, President Muhammadu Buhari wins.

On the other hand, private sector-led growth, driven by revenue optimisation and IMF support, would ensue if the opposition leader, Atiku Abubakar, wins.

Rewane noted that research also indicates that when a younger candidate with energy wins, economies recover as well.

In the event of a deadlock, Afrinvest chief executive officer, said there would be slowdown in economic activities, disruptions to pipelines and insurgency attacks and likely recession driven by exodus of FPIs.

Equally, a deadlock, according to him, would likely result in agitations in the Niger Delta region and drastic decline in oil production due to disruptions to pipelines and force majeure.

Running short of weighing their scenarios in favour of either party, researchers at Afrinvest, West Africa’s leading independent investment banking firm, in an outlook for 2019, titled ‘On the Precipice’, expect possible scenarios amidst the various risk factors envisaged for equity investing in 2019.

The report conceptualised three major possible outcomes that could play out, irrespective of the winner of the presidential election: the pessimistic case, the base case, and the optimistic case.

On the pessimistic case, Afrinvest says there could be a 40 percent probability of post-election violence, which could bring about slower than expected pace of economic growth.

“Our pessimistic case with a probability of 40 percent envisions a likely post-election violence characterised by slower than expected pace of economic growth in addition to negative signals in monetary policy management and increased pace of policy normalisation, especially from the Bank of England (BoE).

“We estimate that this scenario would necessitate at least 20.0 percent decline in market EPS and force P/E as low as 6.7x; hence, crystallising in 33.4 percent decline in the broader index by year end,” they posited.

In the event that the status quo is maintained in major policy disposition with successful and violence-free elections, irrespective of the winner, according to them, would result in a base case.

“Our scenario also envisages that the country maintains slow but steady economic growth path with fiscal and monetary policy conditions subsisting while current pace of global policy normalisation remains.

“In our analysis, this scenario would result in a 6.8 percent EPS growth with higher market P/E (11.4x) resulting in 42.0 percent market return. We believe the possibility of this occurrence is most plausible at 50.0 percent.”

In the optimistic case, which they claim is the least likely on a probability of 10.0 percent, given the current realities, they believe a change in monetary and fiscal policy to drive investments would improve macroeconomic fundamentals.

“This scenario would be most bullish for equities if combined with liberalisation of downstream oil and gas sector, new big listings on the NSE (including MTN) and weaker than expected global growth that could reverse the current course of policy normalisation. This we estimate would result in 15.0 percent growth in EPS with estimated market P/E at 15.2x and market return of 117.7 percent.”

This article was originally published on independent.ng.